Access Control

Access Control Smart Sensors And Automation

Smart Sensors And Automation Network Adapters and Accessories

Network Adapters and Accessories PoE Switches

PoE Switches Point To Point Wireless Radio

Point To Point Wireless Radio Routers

Routers

IP Cameras

IP Cameras Memory Cards

Memory Cards NVR

NVR Smart WiFi Cameras

Smart WiFi Cameras

Desktop & Laptop RAMs

Desktop & Laptop RAMs Internal and External Hard Drives

Internal and External Hard Drives NAS Storage & Enclosures

NAS Storage & Enclosures SSD and NVMe Drives

SSD and NVMe Drives USB Flash Drives

USB Flash DrivesThe future of Internet Service Providers (ISPs) in India and why selling internet alone is no longer enough

In this issue of Tech Tomorrow, we look at why India’s ISP industry is far from dead, but the traditional ISP business model is, the forces squeezing local operators from every direction, and what the ISPs that survive the next five years will look like. Spoiler: they won’t just sell internet.

Before we dive in, if you're someone who enjoys understanding how technology, business, policy, and infrastructure shape the products and services you use every day, join the community if you haven't already. We publish one in-depth edition every two weeks. And if you're already a subscriber, thank you. Consider forwarding this to someone who'd enjoy thoughtful deep dives into the forces powering the country around them.

Here's the story:

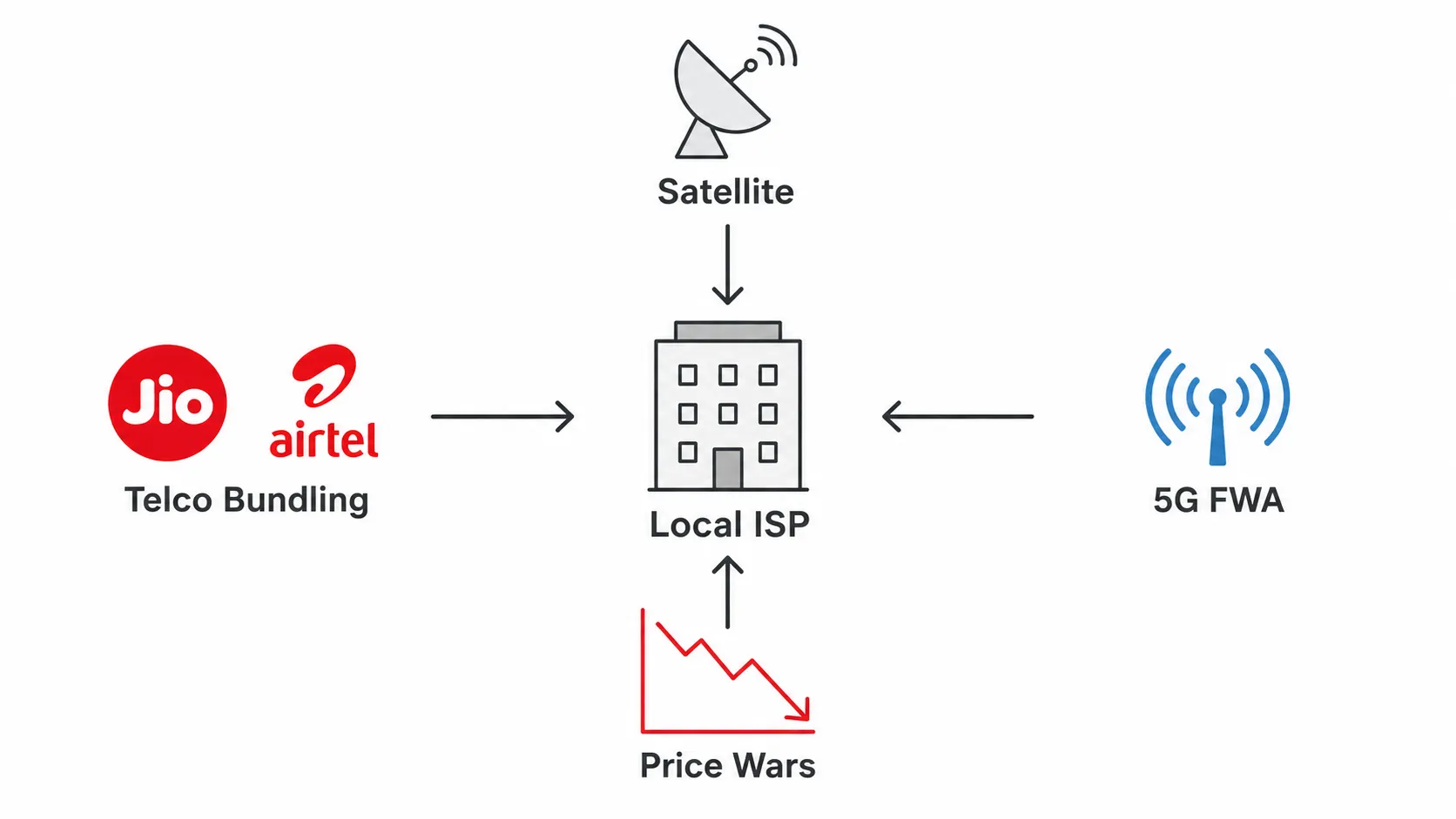

If you run a local ISP in a Tier 2 city, you’ve probably had this experience. You’ve been serving an apartment society for three years. Good uptime, reasonable price, your technician knows the RWA president by name. Then, one quarter, JioFiber shows up. Free installation, bundled OTT apps, a set-top box, and a plan that undercuts yours by ₹200. You lose 40% of the society in two months. So you drop your price. Now you’re running at near-zero margin. Three months later, Airtel Xstream enters the same society. You lose another chunk. This isn’t hypothetical. It’s playing out in thousands of housing societies across India right now. Because here’s the thing, most local ISPs get it wrong about their competition. They think it’s the other fiber operator down the road. It’s not. Their real competition is JioFiber bundling entertainment for free, Airtel rolling out 5G Fixed Wireless Access that doesn’t need a cable, satellite companies preparing to beam internet from space.

But the local ISP model itself? Far from dead.

India’s broadband subscriber base crossed 1.07 billion in April 2026, according to TRAI. The appetite for connectivity keeps climbing.

The problem isn’t demand. The problem is that internet access itself has become a commodity.

When the only question a customer asks is “what’s your monthly price,” the ISP has already lost the margin game. There’s always someone willing to go ₹50 lower. Two operators in the same apartment society end up in a price war until neither makes money.

And that commodity pressure is coming from every direction.

5G Fixed Wireless Access (FWA) is one of the segments to watch. Subscribers more than doubled in under a year, giving customers broadband speeds without trenching, fiber installation, or cable cuts during monsoon season. It won’t replace good fiber networks, but it doesn’t need to. It only needs to be good enough for customers who primarily care about price.

Satellite internet is a longer-term development, but it points in the same direction. When it arrives, it is unlikely to compete with fiber in cities. Instead, it could challenge connectivity providers serving remote villages, industrial sites, farms, and highway locations where laying cable remains difficult.

So if bandwidth is a commodity, if large telcos are bundling aggressively, if FWA is doubling every year, and if satellite is on the horizon, what’s left for the local ISP?

Services.

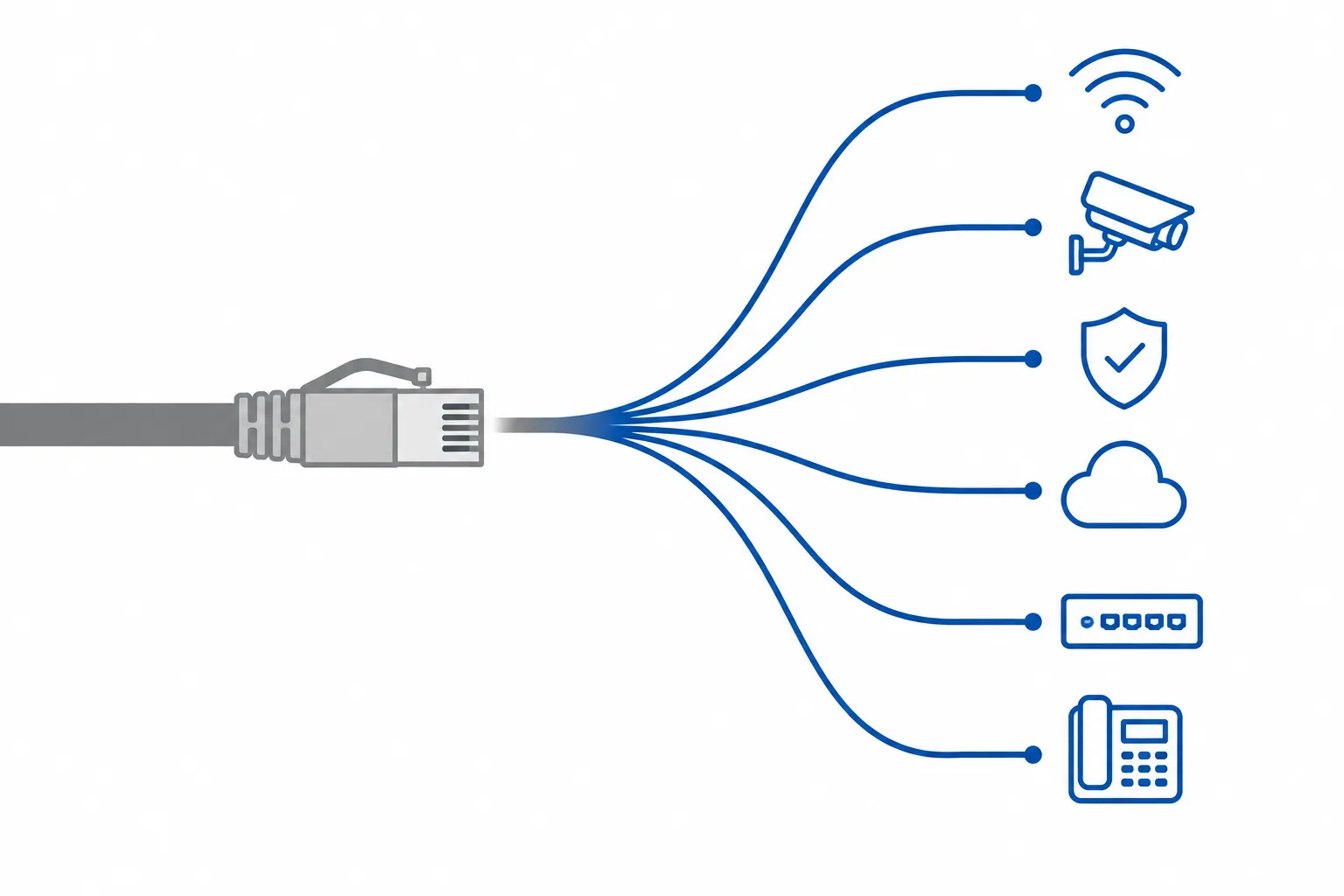

Think about what a typical SMB customer needs.

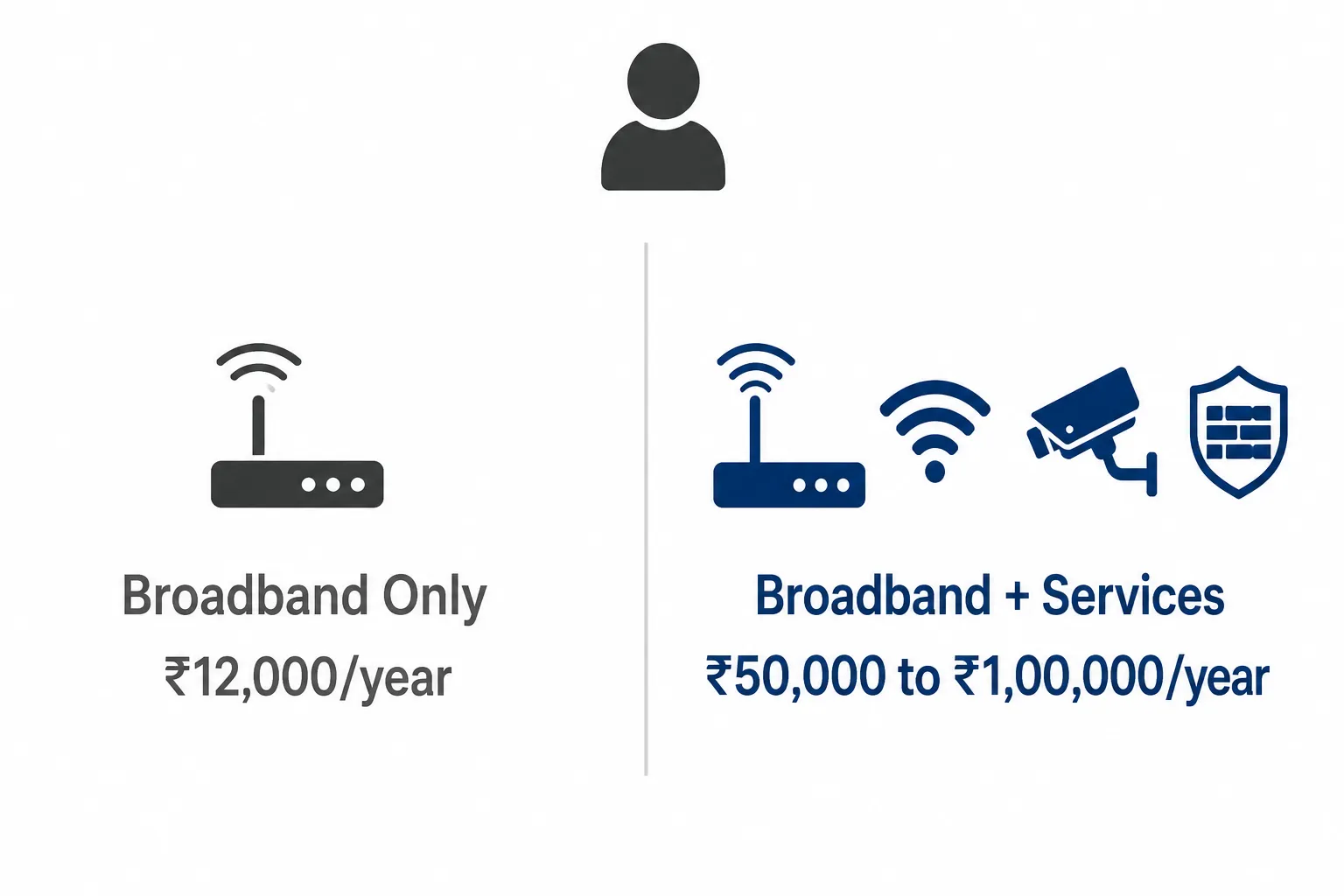

For example, a garment manufacturer doesn’t just need 100 Mbps internet. He needs Wi-Fi that covers his factory floor, eight CCTV cameras with 30-day recording, a firewall that blocks his employees from streaming during work hours, and cloud backup for his Tally data and also needs someone to call immediately when his router stops working. That’s not an internet connection. That’s managed IT.

The ISP that sells him broadband at ₹999 per month earns ₹12,000 a year. The same ISP that sells him broadband plus Wi-Fi management plus CCTV plus a firewall could earn ₹50,000 to ₹1,00,000 a year from the same customer.

Bandwidth margins sit in single digits. Managed service margins can run in the 30 to 40% range. Same customer relationship, completely different economics.

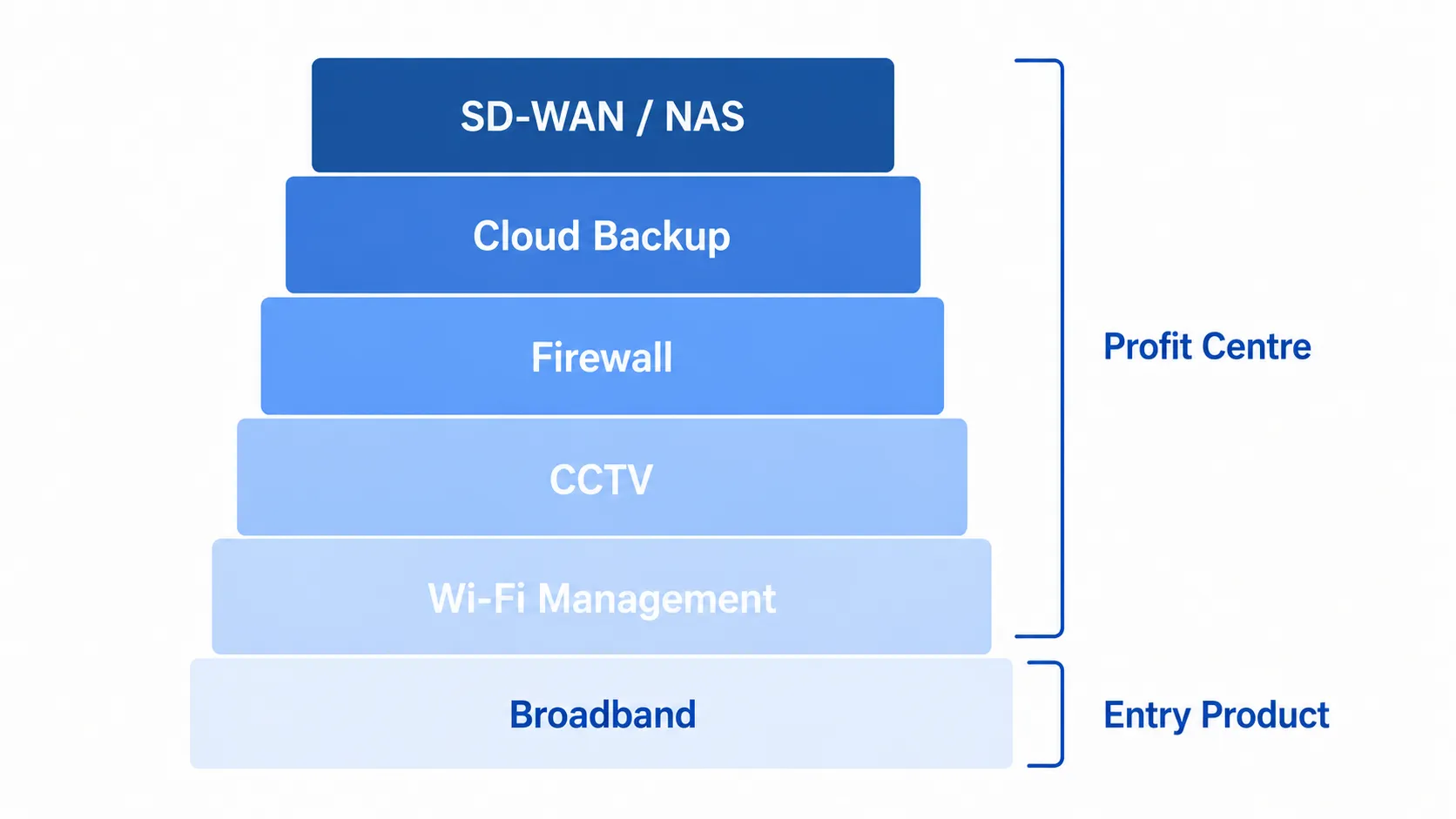

This is the ISP to MSP shift. MSP stands for Managed Service Provider.

The bandwidth becomes the entry product, the thing that gets you in the door. The services on top, Wi-Fi management, CCTV, cybersecurity, cloud backup, SD-WAN, and NAS solutions, become the profit centre

This isn’t a theoretical model; it’s already happening on the ground.

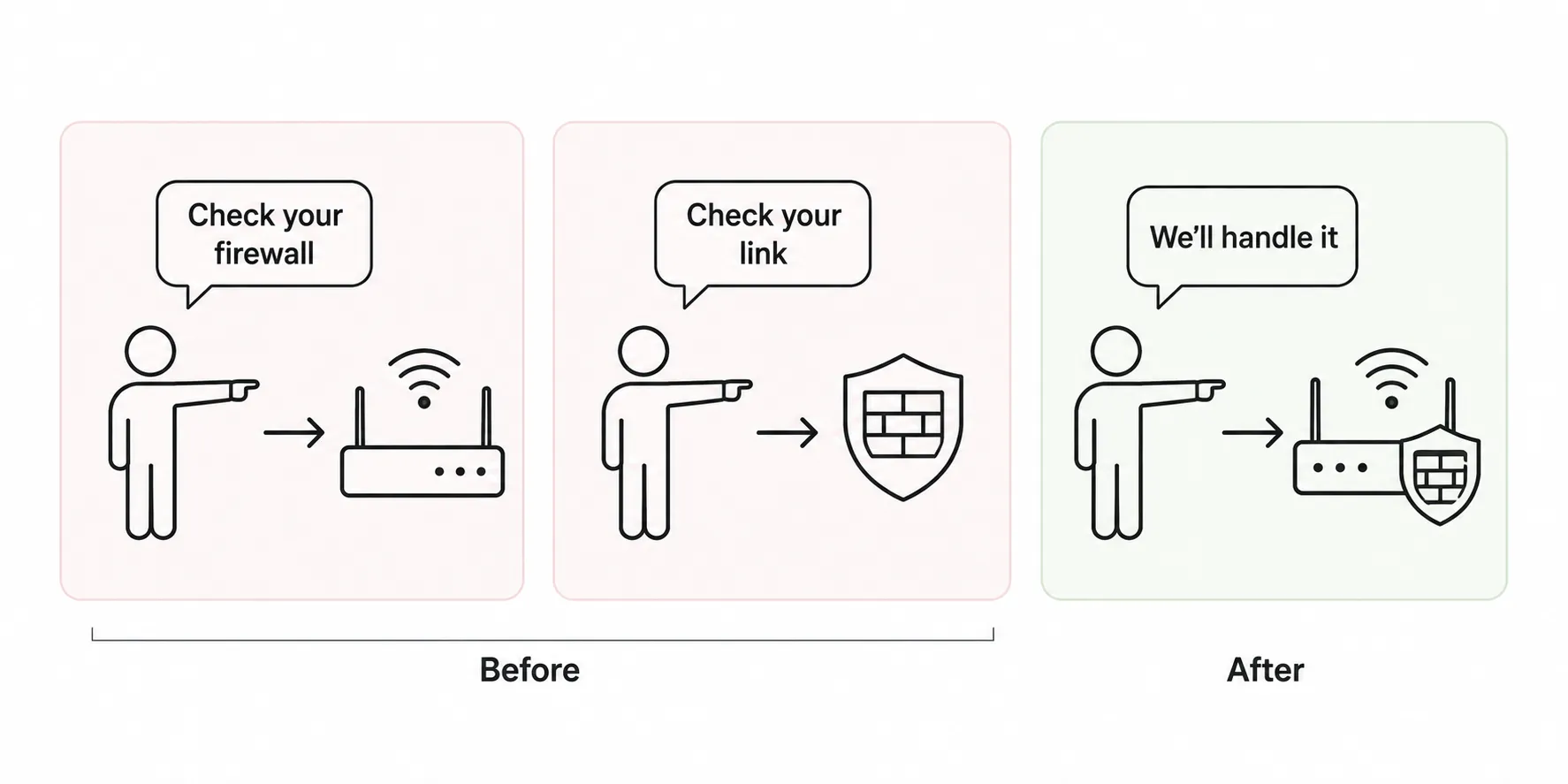

Mr Vikash Sharma, founder of Alliant Technologies, started 11 years ago, selling only broadband and leased lines PAN India for clients in banking, insurance, retail, and hospitality. The internet was their only product. Then they noticed a pattern that anyone who’s worked with multiple vendors will recognise. When a client’s firewall had an issue, the hardware vendor would say, “not my problem, the link is fine.” When the link went down, the ISP would say, “not my problem, check your firewall.” The client was stuck in the middle with nobody owning the problem.

So Alliant started bundling the router and firewall with the connectivity. One provider, one bill, one point of accountability. The blame game disappeared. That bundled approach now accounts for 40% of their business. They went from selling links to selling managed broadband, leased lines, SD-WAN, firewalls, routers, and proactive monitoring through a single dashboard. They even back it with written SLAs, something most providers in this space avoid committing to. And when clients who trusted them with mission-critical connectivity asked “can you handle our Wi-Fi too?”, Alliant added that as well.

And it’s not just established operators making this move.

Roshan Nath, one of our teammates at FGTech, built his own ISP in rural Assam while still in college. He started with a single BSNL AirFiber connection shared with neighbours and grew it to 100 to 150 customers across multiple villages, with over 10 km of fiber laid by hand. But Roshan doesn’t just sell internet anymore. He now sells CCTV solutions, networking hardware, and managed services to both his existing subscriber base and new customers. The ISP gave him the relationships. The products and services gave him the revenue. We wrote about his full journey.

Even brands are recognising this shift.

TP-Link recently launched incentive programs across regions specifically for ISPs willing to sell hardware alongside connectivity. Complete a pre-decided sales target through their distributors, and you earn additional incentives from the brand.

The message is clear: hardware companies want ISPs as their distribution channel because ISPs already have the customer relationship and the last-mile access.

There’s a rural version of this too.

BharatNet, Digital India programs, and state level connectivity projects are bringing more villages online. The ISP that operates in these areas won’t just earn from broadband but from CCTV for panchayat offices, Wi-Fi for digital classrooms, telemedicine connectivity, and smart agriculture sensors. Rural ISPs that position themselves as digital infrastructure companies have a long runway ahead.

But the single biggest opportunity, and the one almost nobody in the ISP conversation is connecting, sits at the intersection of AI, CCTV, and connectivity.

Every AI-powered camera needs bandwidth. It needs storage, either local NAS or cloud. It needs PoE switches to power it. It needs wireless backhaul or fiber links to connect it.

The hardware stack behind a modern surveillance setup is, in many ways, the same stack that ISPs and system integrators already work with. ISPs own the last mile and the customer relationship. CCTV installers own the security relationship.

The overlap between these two businesses is enormous and growing.

One ISP in Ahmednagar, Mr Vicky Khole, reached out to us for a university campus project, a 400-plus hostel room Wi-Fi deployment. He leveraged his existing ISP skills to build a parallel FTTX business and has since expanded into CCTV network management, IP phone intercom setups, and pocket Wi-Fi solutions for students. One customer relationship, five revenue streams, all built on the connectivity foundation he already had.

Interestingly, public policy is still largely focused on expanding access to connectivity itself.

In our previous issue, we wrote about PM-WANI, the government’s scheme to turn chai stalls and kirana stores into public Wi-Fi hotspots selling data sachets. But zoom out and you see a bigger irony. The government is trying to create millions of new pure-bandwidth sellers at the exact moment the market is proving that pure bandwidth selling is a dying business. The demand is there. The model just needs to be services, not sachets.

India has millions of small and medium businesses. Most of them don’t need enterprise IT teams or dedicated network engineers. What they need is one trusted partner who handles their connectivity, their cameras, their storage, their security, and picks up the phone when something breaks.

The ISP that becomes that partner, essentially an outsourced IT department, owns a relationship that Jio and Airtel can't replicate. Because Jio isn't sending a technician to a garment factory within an hour. The local ISP will.

None of this means connectivity-only businesses disappear. Some operators in underserved markets will continue building successful broadband businesses.

The local ISP business in India isn’t dying. The demand for connectivity has never been higher, and it’s still climbing. What’s dying is the traditional model where selling internet access is the entire business. The ISPs that survive the next five years will be the ones who figured out that the connection is just the beginning.

If this made you think about the ISP business differently, share it on WhatsApp, LinkedIn, or X.