Access Control

Access Control Smart Sensors And Automation

Smart Sensors And Automation Network Adapters and Accessories

Network Adapters and Accessories PoE Switches

PoE Switches Point To Point Wireless Radio

Point To Point Wireless Radio Routers

Routers

IP Cameras

IP Cameras Memory Cards

Memory Cards NVR

NVR Smart WiFi Cameras

Smart WiFi Cameras

Desktop & Laptop RAMs

Desktop & Laptop RAMs Internal and External Hard Drives

Internal and External Hard Drives NAS Storage & Enclosures

NAS Storage & Enclosures SSD and NVMe Drives

SSD and NVMe Drives USB Flash Drives

USB Flash DrivesWhen a war 4,000 km away decides what you’ll pay for your next hardware purchase

In this issue, we break down what the US Israel Iran war actually means for networking, storage, and memory hardware prices in India, and why this conflict hits different from any war before it.

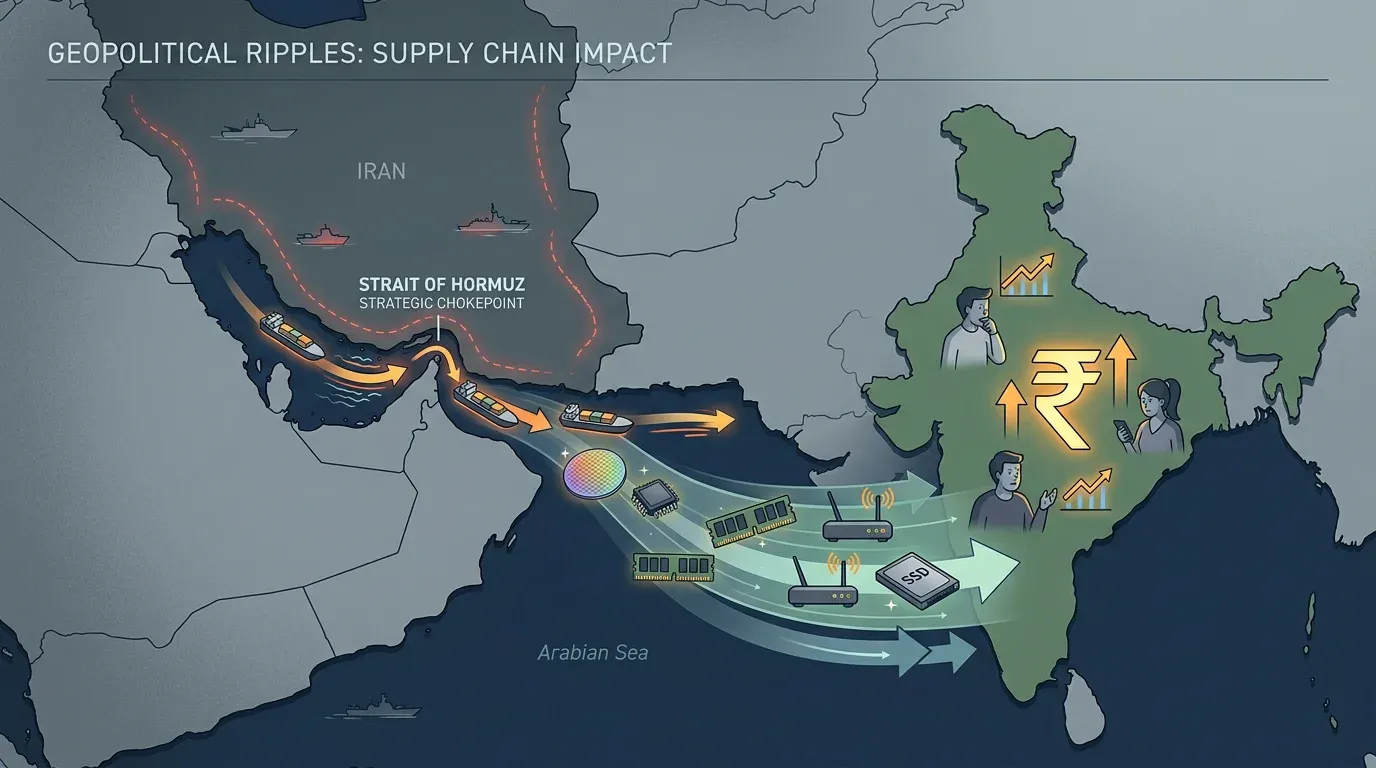

On March 1, 2026, the Strait of Hormuz, a narrow waterway through which half of India’s crude oil passes, was effectively closed to commercial shipping. An Iranian drone had already damaged Qatar’s Ras Laffan helium facility. AWS data centres in the UAE were hit. And suddenly, a war 4,000 km away wasn’t distant at all.

If you work with networking or storage hardware (routers, switches, SSDs, NAS, RAM) this war is about to show up in your price lists. Not tomorrow. But over the next few months, as the supply chain absorbs what’s happening right now.

Here’s the full picture of how it gets from the Gulf to your hardware bill in India

If you read our SSD deep-dive, you already know hardware prices were climbing before any of this. AI data centres had already eaten most of the supply. The war didn't create the crisis; it cut off the fire exits. Here's what the market looked like before the first missile flew:

Think of it like a rice market. Data centres training ChatGPT, Claude, and Gemini are buying 70 out of every 100 bags before they even reach retail. Everyone else (gamers, ISPs, small offices, homelab builders) fights over the remaining 30. Naturally, those bags cost more.

That’s exactly what’s happening with memory chips (DRAM), storage chips (NAND flash), and even the memory inside routers. TrendForce reports that data centres now consume roughly 70% of all memory chips produced globally. Microsoft, Meta, Amazon, and Alphabet alone committed ~$650 billion in data centre spending for 2026.

The result? DRAM prices jumped 90–95% quarter-on-quarter by January 2026. NAND flash for SSDs doubled in six months. Western Digital’s CEO announced in February that the company had sold out its entire 2026 hard drive production to just seven customers; all hyperscalers building AI infrastructure.

That was already the state of the market when the first drone flew and then the war started.

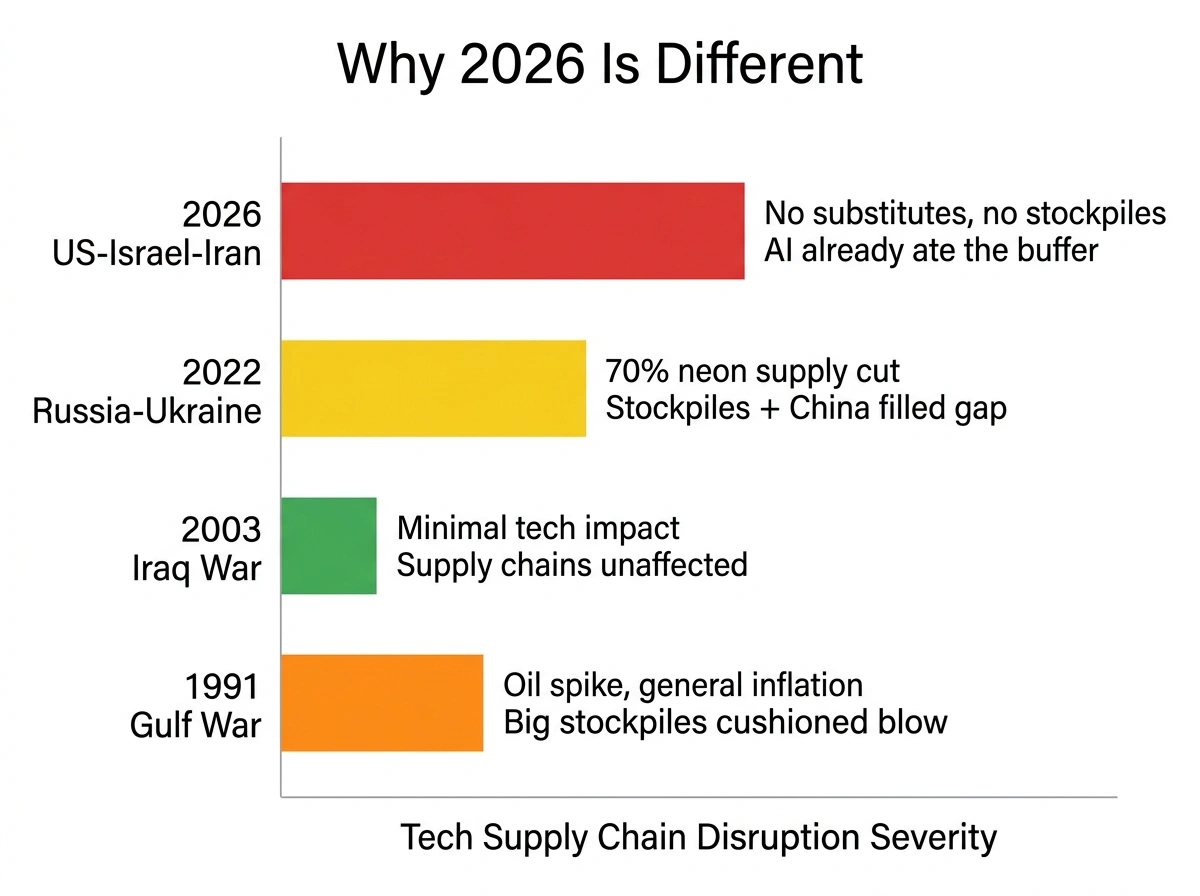

Wars have disrupted tech supply chains before. But 2026 is structurally different.

In 2022, Russia-Ukraine cut off 70% of global neon supply. But chipmakers had stockpiles from after the 2014 Crimea crisis, and China stepped in. The industry absorbed it.

In 2026, there are no such escape routes. Helium, used as a thermal coolant in semiconductor fabrication, has no substitute. On March 2, an Iranian drone strike damaged Qatar’s Ras Laffan facility, which supplies roughly a third of the world’s high-purity helium. Samsung and SK Hynix import nearly two-thirds of their helium from Qatar. Recovery? Experts estimate 6–9 months, minimum.

The war also disrupts bromine, a chemical used in NAND flash production, primarily sourced from Israel and the Dead Sea. Two critical chip materials hit at once.

And it's not just raw materials. Iran has named tech infrastructure as a legitimate target. AWS data centres in the UAE and Bahrain were hit by drone strikes. When a Gulf data centre goes offline, latency and costs ripple through to every Indian business using AWS, Azure, or GCP nodes in the Middle East.

The crucial difference from previous wars: in 2022, chipmakers could lean on inventory buffers. In 2026, those buffers are gone. The AI boom consumed them. Manufacturers are running hand-to-mouth, shipping chips as fast as fabs produce them. When Qatar’s helium supply drops, there’s no cushion.

So how does a US Israel Iran war 4,000 km away reach your local electronics shop in India?

Through three invisible pipelines.

Materials: Helium and bromine are like yeast in bread. You need only a little, but without it, the bakery stops. Chipmakers can’t “work around it”. The chips literally cannot be made the same way.

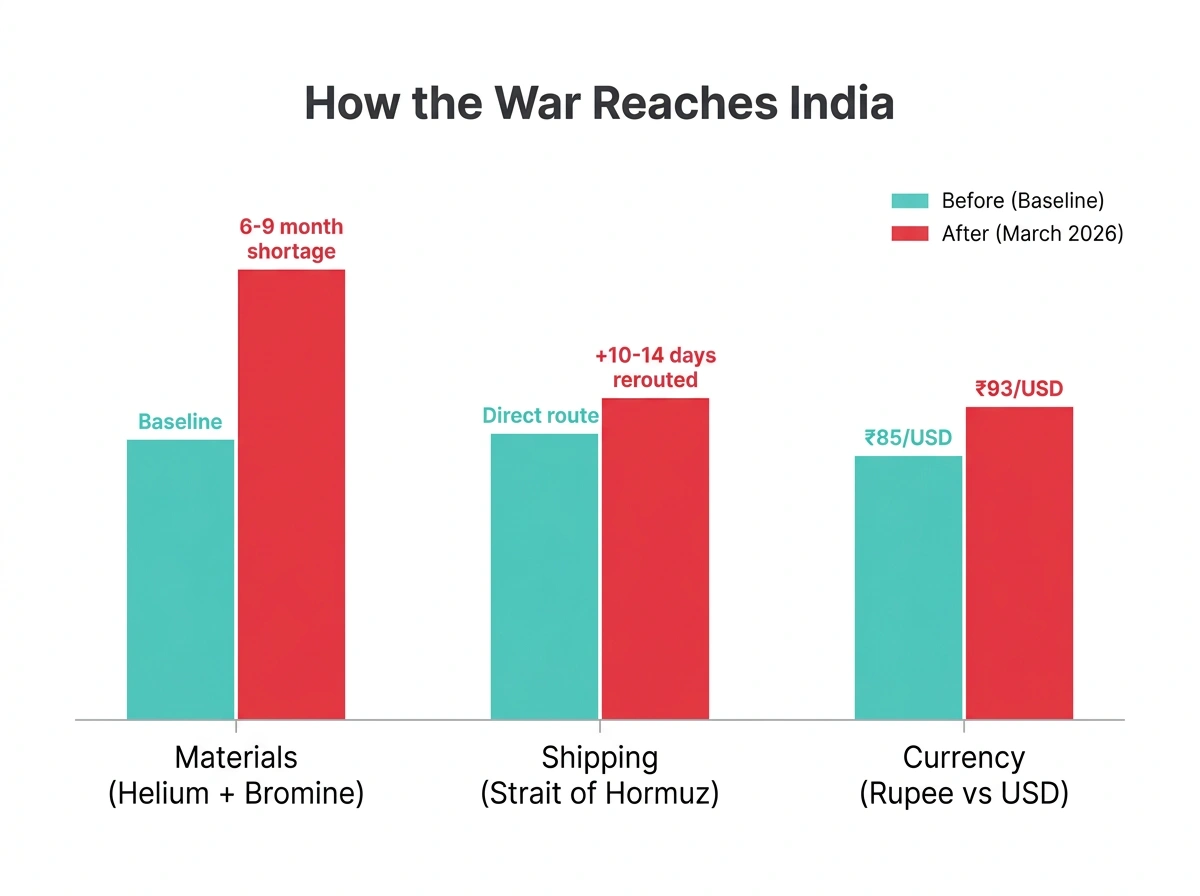

Shipping: The Strait of Hormuz, which carries ~50% of India’s crude oil imports. Ships are rerouting around Africa, adding 10–14 days and significantly higher freight costs to every hardware shipment from Taiwan, South Korea, and China.

Currency: India imports 85% of its crude oil. When Brent crude jumps to $110–120/barrel and half your oil supply is stuck behind a geopolitical bottleneck, the rupee weakens. It’s now above ₹93.5/USD, compared to ₹85–86 a year ago. A $100 product that cost ₹8,500 last year now costs ~₹9,300+, a 10% hike from currency alone

India also exports $4.5 billion worth of electronics to the Gulf annually. With that trade disrupted, freight capacity tightens, and costs rise, which affects inbound hardware shipments too. Economists call it a “double whammy”: oil and shipping costs rising from one direction, the rupee weakening from the other. Even if a product’s dollar price stays flat, it costs more in rupees.

The Indian government has formed an Inter-Ministerial Group specifically to coordinate supply chain resilience, a signal of how seriously officials view the disruption.

Now let’s talk about what this means for the products you buy.

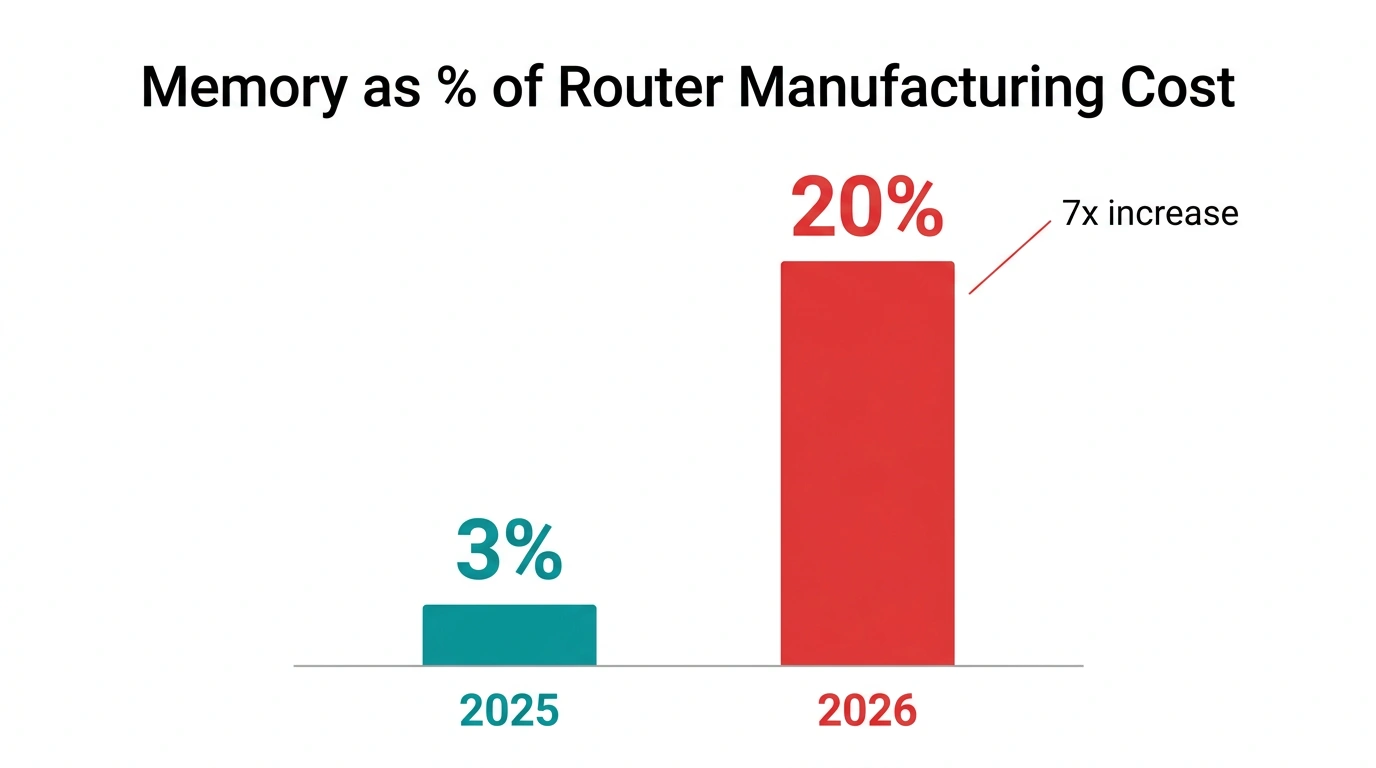

A router is essentially a tiny computer with specialised memory. According to Counterpoint Research, memory now accounts for over 20% of a router’s total manufacturing cost, up from just 3% a year ago. A sevenfold jump. Cisco has already passed these costs through. MikroTik, TP-Link, and Ubiquiti will follow.

For storage, it’s tighter. Western Digital essentially sold its entire 2026 production as a wholesale deal to a handful of AI buyers, leaving retail and SME markets to work with whatever trickles down. Enterprise DDR4 ECC modules that cost ₹6,000–₹8,000 two years ago now run ₹15,000–₹20,000. That’s not a bump; it’s a 3x increase. These are current market prices.

Phison’s CEO, whose company controls roughly 20% of the global SSD controller market, warned recently that entire consumer electronics companies could shut down if memory shortages continue. That's Phison's CEO, a major supplier, saying the pipeline is under serious strain.

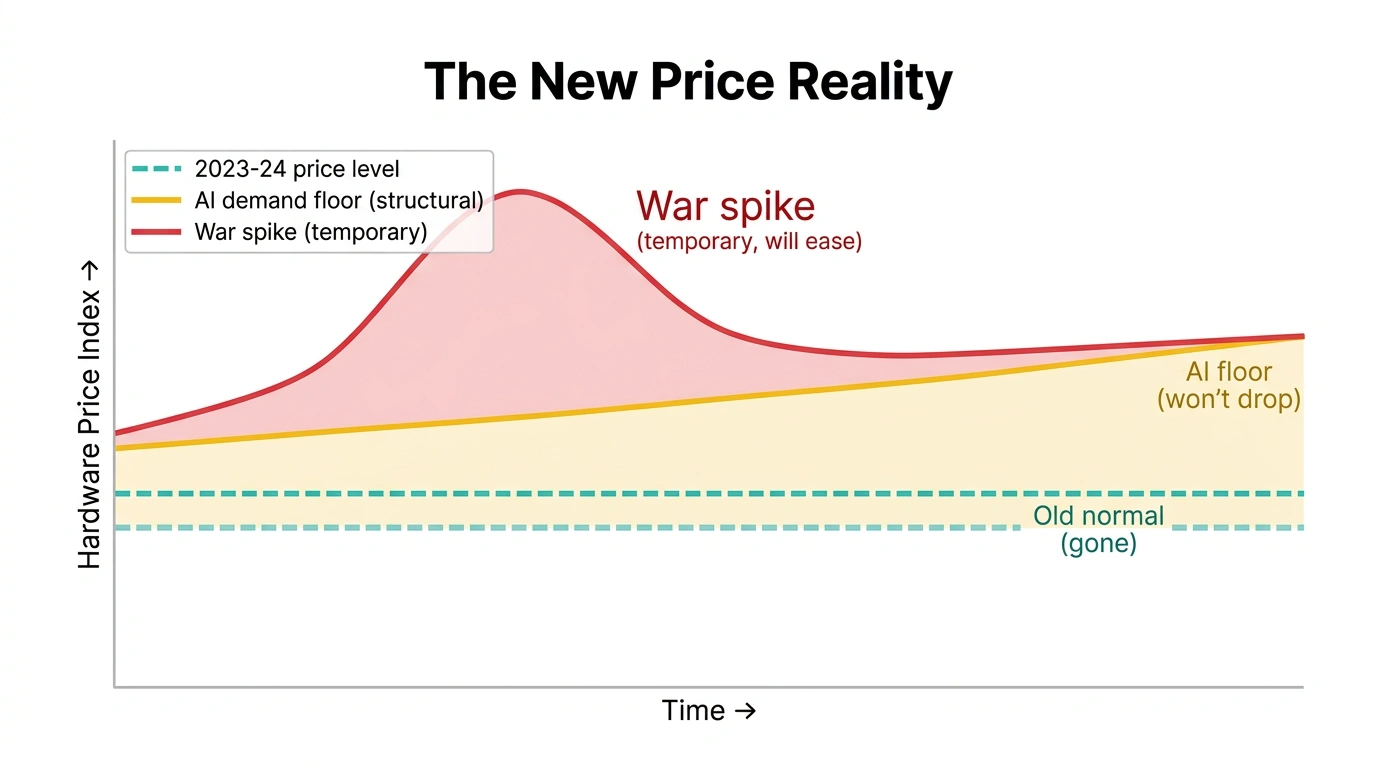

This doesn’t mean everything skyrockets overnight. It means the “new normal” for hardware sits a few steps higher than what buyers got used to in 2022–2023. Memory-heavy gear like switches, NAS boxes, and high-capacity SSDs will see sharper jumps. But almost nothing is getting cheaper.

So what happens when the war ends?

Some of it reverses. Wars end. The Strait reopens. Qatar rebuilds helium capacity (6–9 months, minimum). Shipping routes normalise. The rupee stabilises.

But the structural floor doesn't move. Manufacturers have permanently shifted production toward AI memory. Micron exited consumer memory entirely. IDC and Gartner both expect a new, higher pricing normal, war or no-war.

There's also a delay. Supply chains move in 6–18-month cycles. The shocks from February and March show up in your price list in June.

So the next time a piece of hardware feels oddly expensive, it’s not just markup. It’s AI eating 70% of global memory, helium and bromine supply disruptions, the Strait of Hormuz closure, and a rupee that’s slid from ₹85 to ₹93+.

Before you go...

Hit reply and tell us: Did this change how you think about hardware pricing? What should we break down next: tariffs, chip manufacturing, or something else?